Teva Pharmaceuticals

Tear Sheet: Teva Pharmaceuticals Faces Pressure From Competing Generics, Seeks to Delever Quickly After Actavis Acquisition

Wed 07/05/2017 15:52 PM

Relevant Items:

Link to Reorg Analysis Page for Tear Sheet

Q1 2017 6-K

2016 20-F

Teva 2017 Financial Outlook

Q1 2017 Earnings Presentation

Teva 2016 - 2019 Preliminary Financial Outlook

Teva Pharmaceuticals, which has more than $30 billion of debt accumulated through acquisitions, has so far managed to maintain its investment-grade rating. However, potentially imminent generic competition presents a threat to the company’s most profitable branded drug, Copaxone. The Israel-headquartered pharmaceutical company’s prominent generic drugs business is under deflationary pressures driven by industrywide consolidation. Teva is also facing negative overhang from a regulatory environment that is intent on ramping up generic drug approvals in order to subdue skyrocketing drug prices.

Historically, the company has been supported by stable cash generation and a global footprint allowing for diversification as the world’s largest maker of generic drugs. It has also pursued an aggressive deleveraging timeline communicated by management and required by bank debt covenants.

Teva’s net debt-to-adjusted-EBITDA ratio was 4.5x as of the first quarter 2017, fueled in large part by the transformational acquisition of Actavis Generics in 2016, which received lengthy antitrust scrutiny by the U.S. Federal Trade Commission. The company’s bank debt covenants require a net debt-to-EBITDA ratio below 5.25x, which steps down to 4.25x after this year, according to management. “We see no problems or issues to comply with that,” management said, noting that the company sees “no need to renegotiate or negotiate the covenants.”

Despite management’s confidence in Teva’s ability to meet the covenants laid out in the company’s debt documents, the enhanced leverage profile places an increased burden on the company to continue generating cash flow with much less room for error in execution.

The company’s capital structure is pictured below:

As the company aims to prudently manage its balance sheet to maintain its investment-grade status, the recent trends in its generics business and potential pressures on Copaxone, an injectable prescription medicine used for the treatment of people with relapsing forms of multiple sclerosis, have caught the focus of investors.

Copaxone

Copaxone is a crucial component and primary element of Teva’s specialty pharmaceuticals segment. Teva’s revenue and operating margin are heavily affected by the product, and the company has worked to fight off generic competition and new entrants that threaten to erode Copaxone’s market share. As of the first quarter, Copaxone accounted for 17% of Teva’s consolidated revenue, and management indicated that the product represented 40% of its operating profit excluding G&A.

After generic competition threatened to impede the success of Teva’s 20 mg product, the company artfully launched a 40 mg version, which the market has generally acknowledged is a success. Patients tend to prefer the 40 mg version of the product, however that product now faces the threat of potential new entrants. In January, a court ruling invalidated Teva’s asserted claims of four patents on the 40 mg version of Copaxone, and despite the company’s appeal of the decision, the path to a generic alternative appears to be in sight. Teva management highlighted at a recent conference five filers of potentially competitive products.

In the past, management has provided estimates to assess the potential impact of new generic alternatives to Copaxone, although those estimates have been questioned by analysts on recent earnings calls. As shown below, and as pictured in a presentation for the company’s 2017 outlook, management has reiterated the expectation that two generic competitors to the Copaxone 40 mg product could affect Teva’s top line by more than $1 billion.

Copaxone revenue declined slightly during the first three months of 2017, as did revenue of other products in the specialty pharma segment, mostly as a result of the loss of exclusivity for Nuvigil and Azilect, management said on its first-quarter earnings call. The company’s historical reliance on Copaxone served as one of the drivers behind Teva’s transformative acquisition of Actavis Generics from Allergan, as the company looked to diversify its product portfolio. Although Copaxone continues to have a disproportionate impact on Teva’s financials, Teva’s generics segment accounted for 54% of total consolidated revenue. A breakdown of revenue from the company’s most recent earnings presentation is shown below:

Actavis Acquisition

In July 2015, Teva entered into an agreement to purchase Allergan’s generic pharmaceuticals business, Actavis Generics, using cash of $33.5 billion and approximately 100 million Teva shares. These shares were valued at over $5 billion when the deal closed in August 2016 but are valued at closer to $3 billion as of Monday’s closing price of $33.30 per share. Teva’s stock trades on the Tel Aviv Stock Exchange, and its ADR shares trade under the ticker TEVA on the NYSE.

The transformational combination was meant to create an unparalleled platform of complementary products and a “best-in-class” generics pipeline, albeit at a high cost. The combined generic platform has the top market position in the United States and Europe. Teva has highlighted a robust pipeline of generic products that the company says can contribute meaningfully to top-line growth of the segment. Initial company estimates suggested that new U.S. generic product launches could generate $750 million of additional revenue, however the company clarified during its earnings call for the first quarter of 2017 that revenue in excess of $500 million was more speculative and depended on Teva’s execution over a more risky basket of products.

Although the transaction required considerable external financing, it bolstered Teva’s industry-leading generics business, and management argued at the time of the acquisition that the combination would lead to $1.4 billion of cost synergies and tax savings by the end of 2019, along with a 9.3% return on invested capital. Given Teva’s sizable legacy generics segment, at the time of the acquisition, the company was seen as one of a handful that could have acquired the Actavis generics business during this period of industry consolidation, a move that had the potential for cost savings over the combined platform. Synergy projections from the company’s 2016 - 2019 preliminary financial outlook are shown below.

The product overlap and requirement for approval from the U.S. Federal Trade Commission forced Teva to divest assets. Proceeds would be used by management to pay down the debt incurred. When combining organic cash flow generation and divestiture proceeds, Teva, pro forma the acquisition, expected to generate over $25 billion of free cash flow through 2019 as shown below.

The company provided a revised 2017 cash flow outlook in early 2017, as shown below. Note that free cash flow includes proceeds from divestitures.

Deflationary Headwinds

In the aftermath of Teva’s debt-heavy acquisition of Actavis Generics, heightened deflationary pressure across the generic drug industry represents an ongoing difficulty for the company. Teva’s management has commented on the issue during earnings calls and at various conferences, and pricing pressure for generic drugs has been central to discussions about financial erosion at one of the nation’s largest drug distributors, Cardinal Health. For 2017, Cardinal expects low-double-digit declines in profit for its pharmaceutical segment compared with the prior year, driven by pricing pressure. Cardinal, however, expects deflation in the low double-digits.This aligns with Teva’s forecasts, which had previously called for lighter erosion of 5%. Cardinal’s competitor, AmerisourceBergen, expects deflation in generic drug pricing of 7% to 9% for fiscal year 2017.

Teva has attributed steeper price erosion to the consolidation of its key customers and the increase in generic drug approval by the U.S. Food and Drug Administration, which has created additional competition. Regarding consolidation, the number of players in the supply chain that obtain generic drugs from manufacturers and supply to consumers has shrunk, as the largest drug wholesalers and distributors, pharmacy benefit managers and retail pharmacies continue to align to amass purchasing power in negotiations with companies such as Teva. These consortiums have led to questions for Teva about further downticks in generic pricing, as the consortiums largely represent the buying base for Teva’s generic drugs. Teva’s management has noted that four “group purchasing organizations” account for more than 80% of generic drug purchases. The generic drug price erosion that Teva experienced in the first quarter was driven by that consolidation, management said.

AmerisourceBergen, for example, recently reached a new five-year agreement to supply pharmaceuticals to the pharmacy benefit manager Express Scripts. AmerisourceBergen also has a generic distribution contract with retail pharmacy Walgreens, through which AmerisourceBergen is able to distribute generic drugs to Walgreens’ extensive network of retail stores, mail order and specialty pharmacies. Walgreens is part of Express Scripts’ network, and Express Scripts operates its own mail-order pharmacy. Similar alliances have popped up among and between Cardinal Health, OptumRX, and CVS retail pharmacies, as well as the McKesson Corporation, the CVS/caremark prescription benefit manager, and Wal-Mart.

Regarding the U.S. Food and Drug Administration, last year the agency set a record for its generic drug program. In 2016, the FDA’s Office of Generic Drugs, or OGD, generated more than 800 generic drug approvals, the highest number in the history of the FDA’s generic drug program, according to a February post on the FDA’s blog. Many of these approvals were for “first-time generic drugs,” meaning the introduction of a generic counterpart for a brand-name product for which there was previously no generic, according to the post. Recent commentary and steps taken by the FDA indicate that generic approval will not be slowing down anytime soon.

President Donald Trump’s FDA commissioner Scott Gottlieb noted in his first remarks to the agency on May 15 that drug pricing would be a priority for the agency. “For one thing, too many consumers are priced out of the medicines they need. Now, I know FDA doesn’t play a direct role in drug pricing. But we still need to be taking meaningful steps to get more low cost alternatives to the market, to increase competition, and to give consumers more options,” he said, adding that the FDA must take steps to ensure that the generic drug process isn’t being “inappropriately gamed” to delay competition and disadvantage consumers.

On June 27, the FDA published a list of off-patent, off-exclusivity branded drugs that currently lack generic competition. The agency posted the list to encourage generic drug development and approval of generic drug applications, known as Abbreviated New Drug Applications, or ANDAs. The FDA intends to expedite the review of any generic drug application for a product on the list to ensure that they come to market as quickly as possible, according to the news release publicizing the list. The FDA will refine and update the list periodically to “ensure continued transparency around drug categories where increased competition has the potential to provide significant benefit to patients,” according to the news release.

When it released the list, the FDA announced a change to its policy regarding how it prioritizes the review of generic drug applications. The FDA will expedite the review of generic drug applications until there are three approved generics for a given drug product, according to the same press release. The agency is revising the policy on the basis of data indicating that consumers see significant price reductions when there are multiple FDA-approved generics available, according to the release. “These are the first of a series of steps the agency intends to take to help tackle this important issue,” the release states.

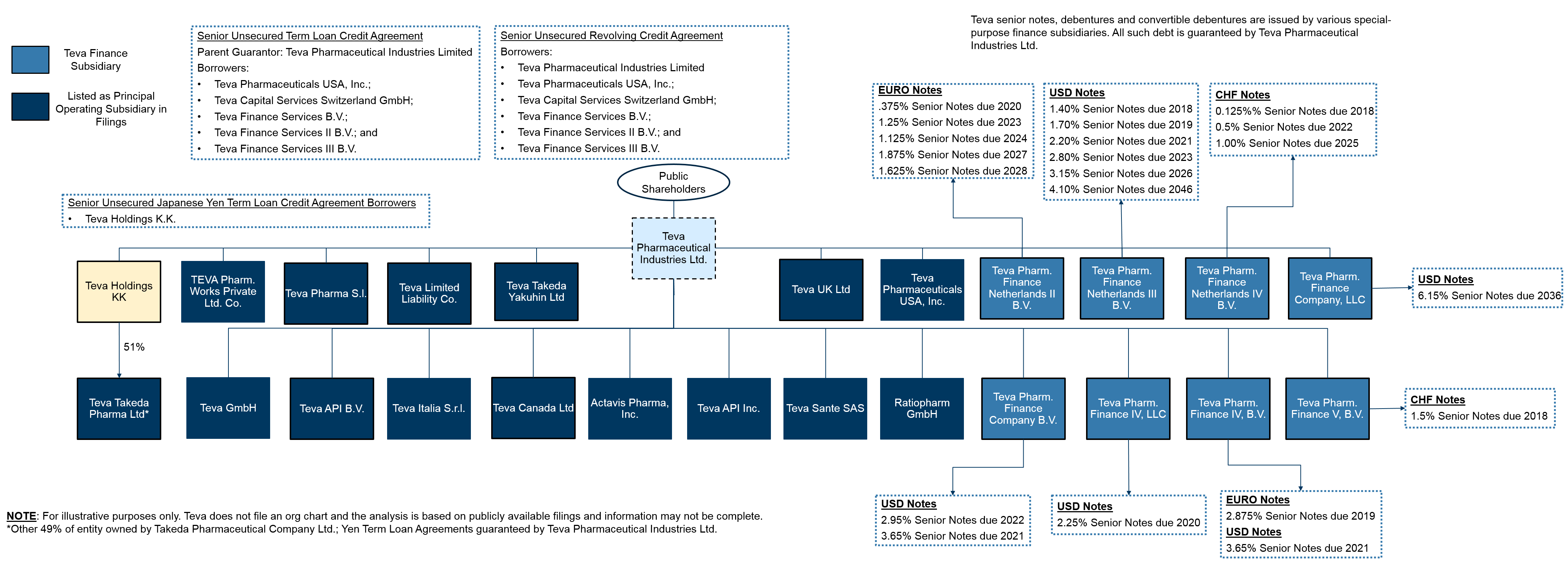

Capital Structure and Organizational Chart

The acquisition of Actavis vastly altered Teva’s capitalization and leverage profile, as highlighted by the company in recent earnings presentations as shown below.

Teva has a complex capital structure with tranches of debt comprising both bank loans and bonds denominated in four different currencies. Teva financed the acquisition of Actavis Generics with more than $20 billion of senior notes offered in U.S. dollars, euros and Swiss francs, proceeds from the offering of new shares and mandatorily convertible preferred shares, cash on hand and borrowings under both a new term loan facility and short-term credit facility. An illustrative organizational chart for Teva is shown below:

(Click on image to enlarge)

Upon the closing of the Actavis Generics transaction, Teva and certain subsidiaries entered into a $4.5 billion senior unsecured revolving credit agreement and a $5 billion unsecured term loan facility that includes two tranches totaling $2.5 billion. The first tranche of $2.5 billion has a three-year maturity, and the entire balance is due in November 2018. The second tranche has a five-year maturity and requires principal installments of $250 million, $250 million, $500 million and $500 million on each anniversary of the borrowing, with a final $1 billion payment in November 2020. Both the unsecured revolving credit facility and term loan facility credit agreements were among Teva Pharmaceutical Industries Ltd., as the parent guarantor, and Teva Pharmaceuticals USA Inc., Teva Capital Services Switzerland GMBH, Teva Finance Services BV, Teva Finance Services II BV, Teva Finance Services III BV as borrowers.

A subsidiary of Teva, Teva Holdings KK, has entered into multiple senior unsecured Japanese yen term loan credit agreements, which are guaranteed by Teva Pharmaceutical Industries Ltd. Teva Holdings KK owns 51% of Teva Takeda Pharma Ltd., a business venture between Teva and Takeda Pharmaceutical Company Ltd., among other assets.

Teva’s unsecured bank facilities contain financial covenants including a maximum consolidated net leverage covenant and a minimum interest coverage ratio covenant. The net leverage covenant was set at 5.25x for the first full quarter of its issuance (the fourth quarter of 2016), and it steps down as shown below:

The interest coverage ratio is set at 3.5x and does not fluctuate. In addition, as noted in Teva’s financial statements, “the company and certain subsidiaries entered into negative pledge agreements with certain banks and institutional investors. Under the agreements, the company and such subsidiaries have undertaken not to register floating charges on assets in favor of any third parties without the prior consent of the banks.”

The company’s senior notes and debentures have been issued as unsecured senior obligations by various special-purpose finance subsidiaries and are guaranteed by parent Teva Pharmaceutical Industries Ltd., making them unsecured senior obligations of the parent entity.

Teva management has outlined a rather aggressive schedule to pay down debt to delever the business. The company eliminated nearly $1.1 billion of net debt during the first quarter of fiscal 2017.

Management Instability

After three years as CEO, Erez Vigodman stepped down from his position in February as Teva faced enhanced scrutiny stemming from the headwinds highlighted above. He was replaced by chairman Yitzhak Peterburg on an interim basis, and former Celgene Corp CEO Sol Barer took over the position of chairman of the board of directors. The departure of Vigodman was followed by the departure of CFO Eyal Desheh in April.

Although Peterburg and Barer have reiterated their commitment to conducting a comprehensive overview of the company’s positioning, the inability to fill these integral C-suite positions has remained a central focus of analysts on recent earnings calls and during recent conferences. The interim management team has highlighted the understanding that new leadership must have both a solid knowledge of the pharmaceutical industry and the ability to conduct a transformative strategic restructuring. As noted by Peterburg at a recent conference in early June:

“We have a search committee led by our Chairman, Sol Barer, and another two Board members. They are working as we speak.

“The profile of the next CEO was defined by the Board. And answering one your questions is we clearly said that what we expect the next CEO to be is, first of all, be a CEO level today with a very - really important background in pharma. Based on the question you asked about the prior one, we felt it was very, very important. But this is not enough by itself.

“And we ask that at the same time whoever will come, he or she - in the minute I will explain where we are in the process - will have the ability to maybe do the restructuring needed, being able to deal with change and with the [deceptions] that we think are within our industry.”

Link to Reorg Analysis Page for Tear Sheet

Q1 2017 6-K

2016 20-F

Teva 2017 Financial Outlook

Q1 2017 Earnings Presentation

Teva 2016 - 2019 Preliminary Financial Outlook

Teva Pharmaceuticals, which has more than $30 billion of debt accumulated through acquisitions, has so far managed to maintain its investment-grade rating. However, potentially imminent generic competition presents a threat to the company’s most profitable branded drug, Copaxone. The Israel-headquartered pharmaceutical company’s prominent generic drugs business is under deflationary pressures driven by industrywide consolidation. Teva is also facing negative overhang from a regulatory environment that is intent on ramping up generic drug approvals in order to subdue skyrocketing drug prices.

Historically, the company has been supported by stable cash generation and a global footprint allowing for diversification as the world’s largest maker of generic drugs. It has also pursued an aggressive deleveraging timeline communicated by management and required by bank debt covenants.

Teva’s net debt-to-adjusted-EBITDA ratio was 4.5x as of the first quarter 2017, fueled in large part by the transformational acquisition of Actavis Generics in 2016, which received lengthy antitrust scrutiny by the U.S. Federal Trade Commission. The company’s bank debt covenants require a net debt-to-EBITDA ratio below 5.25x, which steps down to 4.25x after this year, according to management. “We see no problems or issues to comply with that,” management said, noting that the company sees “no need to renegotiate or negotiate the covenants.”

Despite management’s confidence in Teva’s ability to meet the covenants laid out in the company’s debt documents, the enhanced leverage profile places an increased burden on the company to continue generating cash flow with much less room for error in execution.

The company’s capital structure is pictured below:

As the company aims to prudently manage its balance sheet to maintain its investment-grade status, the recent trends in its generics business and potential pressures on Copaxone, an injectable prescription medicine used for the treatment of people with relapsing forms of multiple sclerosis, have caught the focus of investors.

Copaxone

Copaxone is a crucial component and primary element of Teva’s specialty pharmaceuticals segment. Teva’s revenue and operating margin are heavily affected by the product, and the company has worked to fight off generic competition and new entrants that threaten to erode Copaxone’s market share. As of the first quarter, Copaxone accounted for 17% of Teva’s consolidated revenue, and management indicated that the product represented 40% of its operating profit excluding G&A.

After generic competition threatened to impede the success of Teva’s 20 mg product, the company artfully launched a 40 mg version, which the market has generally acknowledged is a success. Patients tend to prefer the 40 mg version of the product, however that product now faces the threat of potential new entrants. In January, a court ruling invalidated Teva’s asserted claims of four patents on the 40 mg version of Copaxone, and despite the company’s appeal of the decision, the path to a generic alternative appears to be in sight. Teva management highlighted at a recent conference five filers of potentially competitive products.

In the past, management has provided estimates to assess the potential impact of new generic alternatives to Copaxone, although those estimates have been questioned by analysts on recent earnings calls. As shown below, and as pictured in a presentation for the company’s 2017 outlook, management has reiterated the expectation that two generic competitors to the Copaxone 40 mg product could affect Teva’s top line by more than $1 billion.

Copaxone revenue declined slightly during the first three months of 2017, as did revenue of other products in the specialty pharma segment, mostly as a result of the loss of exclusivity for Nuvigil and Azilect, management said on its first-quarter earnings call. The company’s historical reliance on Copaxone served as one of the drivers behind Teva’s transformative acquisition of Actavis Generics from Allergan, as the company looked to diversify its product portfolio. Although Copaxone continues to have a disproportionate impact on Teva’s financials, Teva’s generics segment accounted for 54% of total consolidated revenue. A breakdown of revenue from the company’s most recent earnings presentation is shown below:

Actavis Acquisition

In July 2015, Teva entered into an agreement to purchase Allergan’s generic pharmaceuticals business, Actavis Generics, using cash of $33.5 billion and approximately 100 million Teva shares. These shares were valued at over $5 billion when the deal closed in August 2016 but are valued at closer to $3 billion as of Monday’s closing price of $33.30 per share. Teva’s stock trades on the Tel Aviv Stock Exchange, and its ADR shares trade under the ticker TEVA on the NYSE.

The transformational combination was meant to create an unparalleled platform of complementary products and a “best-in-class” generics pipeline, albeit at a high cost. The combined generic platform has the top market position in the United States and Europe. Teva has highlighted a robust pipeline of generic products that the company says can contribute meaningfully to top-line growth of the segment. Initial company estimates suggested that new U.S. generic product launches could generate $750 million of additional revenue, however the company clarified during its earnings call for the first quarter of 2017 that revenue in excess of $500 million was more speculative and depended on Teva’s execution over a more risky basket of products.

Although the transaction required considerable external financing, it bolstered Teva’s industry-leading generics business, and management argued at the time of the acquisition that the combination would lead to $1.4 billion of cost synergies and tax savings by the end of 2019, along with a 9.3% return on invested capital. Given Teva’s sizable legacy generics segment, at the time of the acquisition, the company was seen as one of a handful that could have acquired the Actavis generics business during this period of industry consolidation, a move that had the potential for cost savings over the combined platform. Synergy projections from the company’s 2016 - 2019 preliminary financial outlook are shown below.

The product overlap and requirement for approval from the U.S. Federal Trade Commission forced Teva to divest assets. Proceeds would be used by management to pay down the debt incurred. When combining organic cash flow generation and divestiture proceeds, Teva, pro forma the acquisition, expected to generate over $25 billion of free cash flow through 2019 as shown below.

The company provided a revised 2017 cash flow outlook in early 2017, as shown below. Note that free cash flow includes proceeds from divestitures.

Deflationary Headwinds

In the aftermath of Teva’s debt-heavy acquisition of Actavis Generics, heightened deflationary pressure across the generic drug industry represents an ongoing difficulty for the company. Teva’s management has commented on the issue during earnings calls and at various conferences, and pricing pressure for generic drugs has been central to discussions about financial erosion at one of the nation’s largest drug distributors, Cardinal Health. For 2017, Cardinal expects low-double-digit declines in profit for its pharmaceutical segment compared with the prior year, driven by pricing pressure. Cardinal, however, expects deflation in the low double-digits.This aligns with Teva’s forecasts, which had previously called for lighter erosion of 5%. Cardinal’s competitor, AmerisourceBergen, expects deflation in generic drug pricing of 7% to 9% for fiscal year 2017.

Teva has attributed steeper price erosion to the consolidation of its key customers and the increase in generic drug approval by the U.S. Food and Drug Administration, which has created additional competition. Regarding consolidation, the number of players in the supply chain that obtain generic drugs from manufacturers and supply to consumers has shrunk, as the largest drug wholesalers and distributors, pharmacy benefit managers and retail pharmacies continue to align to amass purchasing power in negotiations with companies such as Teva. These consortiums have led to questions for Teva about further downticks in generic pricing, as the consortiums largely represent the buying base for Teva’s generic drugs. Teva’s management has noted that four “group purchasing organizations” account for more than 80% of generic drug purchases. The generic drug price erosion that Teva experienced in the first quarter was driven by that consolidation, management said.

AmerisourceBergen, for example, recently reached a new five-year agreement to supply pharmaceuticals to the pharmacy benefit manager Express Scripts. AmerisourceBergen also has a generic distribution contract with retail pharmacy Walgreens, through which AmerisourceBergen is able to distribute generic drugs to Walgreens’ extensive network of retail stores, mail order and specialty pharmacies. Walgreens is part of Express Scripts’ network, and Express Scripts operates its own mail-order pharmacy. Similar alliances have popped up among and between Cardinal Health, OptumRX, and CVS retail pharmacies, as well as the McKesson Corporation, the CVS/caremark prescription benefit manager, and Wal-Mart.

Regarding the U.S. Food and Drug Administration, last year the agency set a record for its generic drug program. In 2016, the FDA’s Office of Generic Drugs, or OGD, generated more than 800 generic drug approvals, the highest number in the history of the FDA’s generic drug program, according to a February post on the FDA’s blog. Many of these approvals were for “first-time generic drugs,” meaning the introduction of a generic counterpart for a brand-name product for which there was previously no generic, according to the post. Recent commentary and steps taken by the FDA indicate that generic approval will not be slowing down anytime soon.

President Donald Trump’s FDA commissioner Scott Gottlieb noted in his first remarks to the agency on May 15 that drug pricing would be a priority for the agency. “For one thing, too many consumers are priced out of the medicines they need. Now, I know FDA doesn’t play a direct role in drug pricing. But we still need to be taking meaningful steps to get more low cost alternatives to the market, to increase competition, and to give consumers more options,” he said, adding that the FDA must take steps to ensure that the generic drug process isn’t being “inappropriately gamed” to delay competition and disadvantage consumers.

On June 27, the FDA published a list of off-patent, off-exclusivity branded drugs that currently lack generic competition. The agency posted the list to encourage generic drug development and approval of generic drug applications, known as Abbreviated New Drug Applications, or ANDAs. The FDA intends to expedite the review of any generic drug application for a product on the list to ensure that they come to market as quickly as possible, according to the news release publicizing the list. The FDA will refine and update the list periodically to “ensure continued transparency around drug categories where increased competition has the potential to provide significant benefit to patients,” according to the news release.

When it released the list, the FDA announced a change to its policy regarding how it prioritizes the review of generic drug applications. The FDA will expedite the review of generic drug applications until there are three approved generics for a given drug product, according to the same press release. The agency is revising the policy on the basis of data indicating that consumers see significant price reductions when there are multiple FDA-approved generics available, according to the release. “These are the first of a series of steps the agency intends to take to help tackle this important issue,” the release states.

Capital Structure and Organizational Chart

The acquisition of Actavis vastly altered Teva’s capitalization and leverage profile, as highlighted by the company in recent earnings presentations as shown below.

Teva has a complex capital structure with tranches of debt comprising both bank loans and bonds denominated in four different currencies. Teva financed the acquisition of Actavis Generics with more than $20 billion of senior notes offered in U.S. dollars, euros and Swiss francs, proceeds from the offering of new shares and mandatorily convertible preferred shares, cash on hand and borrowings under both a new term loan facility and short-term credit facility. An illustrative organizational chart for Teva is shown below:

(Click on image to enlarge)

Upon the closing of the Actavis Generics transaction, Teva and certain subsidiaries entered into a $4.5 billion senior unsecured revolving credit agreement and a $5 billion unsecured term loan facility that includes two tranches totaling $2.5 billion. The first tranche of $2.5 billion has a three-year maturity, and the entire balance is due in November 2018. The second tranche has a five-year maturity and requires principal installments of $250 million, $250 million, $500 million and $500 million on each anniversary of the borrowing, with a final $1 billion payment in November 2020. Both the unsecured revolving credit facility and term loan facility credit agreements were among Teva Pharmaceutical Industries Ltd., as the parent guarantor, and Teva Pharmaceuticals USA Inc., Teva Capital Services Switzerland GMBH, Teva Finance Services BV, Teva Finance Services II BV, Teva Finance Services III BV as borrowers.

A subsidiary of Teva, Teva Holdings KK, has entered into multiple senior unsecured Japanese yen term loan credit agreements, which are guaranteed by Teva Pharmaceutical Industries Ltd. Teva Holdings KK owns 51% of Teva Takeda Pharma Ltd., a business venture between Teva and Takeda Pharmaceutical Company Ltd., among other assets.

Teva’s unsecured bank facilities contain financial covenants including a maximum consolidated net leverage covenant and a minimum interest coverage ratio covenant. The net leverage covenant was set at 5.25x for the first full quarter of its issuance (the fourth quarter of 2016), and it steps down as shown below:

The interest coverage ratio is set at 3.5x and does not fluctuate. In addition, as noted in Teva’s financial statements, “the company and certain subsidiaries entered into negative pledge agreements with certain banks and institutional investors. Under the agreements, the company and such subsidiaries have undertaken not to register floating charges on assets in favor of any third parties without the prior consent of the banks.”

The company’s senior notes and debentures have been issued as unsecured senior obligations by various special-purpose finance subsidiaries and are guaranteed by parent Teva Pharmaceutical Industries Ltd., making them unsecured senior obligations of the parent entity.

Teva management has outlined a rather aggressive schedule to pay down debt to delever the business. The company eliminated nearly $1.1 billion of net debt during the first quarter of fiscal 2017.

Management Instability

After three years as CEO, Erez Vigodman stepped down from his position in February as Teva faced enhanced scrutiny stemming from the headwinds highlighted above. He was replaced by chairman Yitzhak Peterburg on an interim basis, and former Celgene Corp CEO Sol Barer took over the position of chairman of the board of directors. The departure of Vigodman was followed by the departure of CFO Eyal Desheh in April.

Although Peterburg and Barer have reiterated their commitment to conducting a comprehensive overview of the company’s positioning, the inability to fill these integral C-suite positions has remained a central focus of analysts on recent earnings calls and during recent conferences. The interim management team has highlighted the understanding that new leadership must have both a solid knowledge of the pharmaceutical industry and the ability to conduct a transformative strategic restructuring. As noted by Peterburg at a recent conference in early June:

“We have a search committee led by our Chairman, Sol Barer, and another two Board members. They are working as we speak.

“The profile of the next CEO was defined by the Board. And answering one your questions is we clearly said that what we expect the next CEO to be is, first of all, be a CEO level today with a very - really important background in pharma. Based on the question you asked about the prior one, we felt it was very, very important. But this is not enough by itself.

“And we ask that at the same time whoever will come, he or she - in the minute I will explain where we are in the process - will have the ability to maybe do the restructuring needed, being able to deal with change and with the [deceptions] that we think are within our industry.”

This article is an example of the content you may receive if you subscribe to a product of Reorg Research, Inc. or one of its affiliates (collectively, “Reorg”). The information contained herein should not be construed as legal, investment, accounting or other professional services advice on any subject. Reorg, its affiliates, officers, directors, partners and employees expressly disclaim all liability in respect to actions taken or not taken based on any or all the contents of this publication. Copyright © 2024 Reorg Research, Inc. All rights reserved.